Payment link: what is the best option in France

Discover the link-based payment solution that's right for your business, be it B2C or B2B.

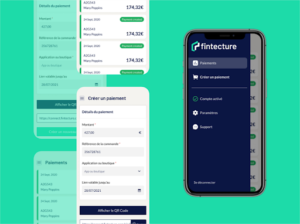

Fintecture, the bank transfer payment solution

Discover the link-based payment solution that's right for your business, be it B2C or B2B.

Discover our examples of dunning letters according to a situation.

Discover instant money transfer in France: fast, secure payments. Complete guide to rates and compatible banks.