Instant money transfer explained: Speed, rates and advantages

Discover instant money transfer in France: fast, secure payments. Complete guide to rates and compatible banks.

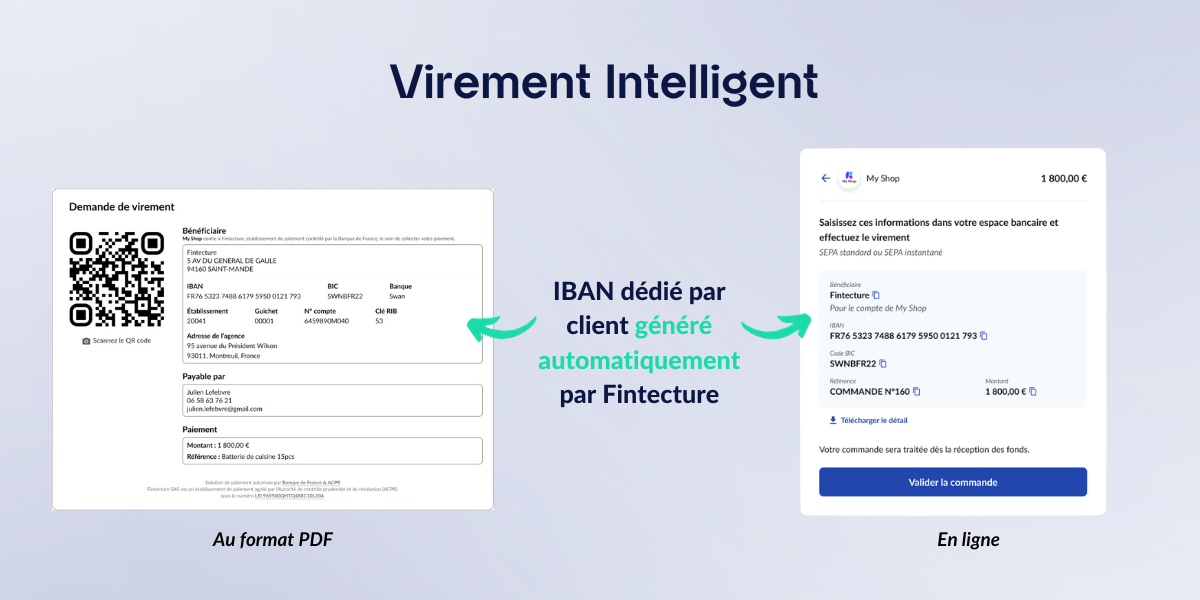

Fintecture, the bank transfer payment solution

Discover instant money transfer in France: fast, secure payments. Complete guide to rates and compatible banks.

Free and convenient for customers, efficient and opportunity-generating for merchants, click & collect has it all!

This €26 million Series A round brings Fintecture's funding to a total of €32 million, following a €6 million round raised in May 2021.