How to reduce your DSO with payment solutions?

DSO (Days Sales Outstanding) indicates the average time taken to pay customers. A high DSO lengthens the settlement time, impacting the company's cash flow.

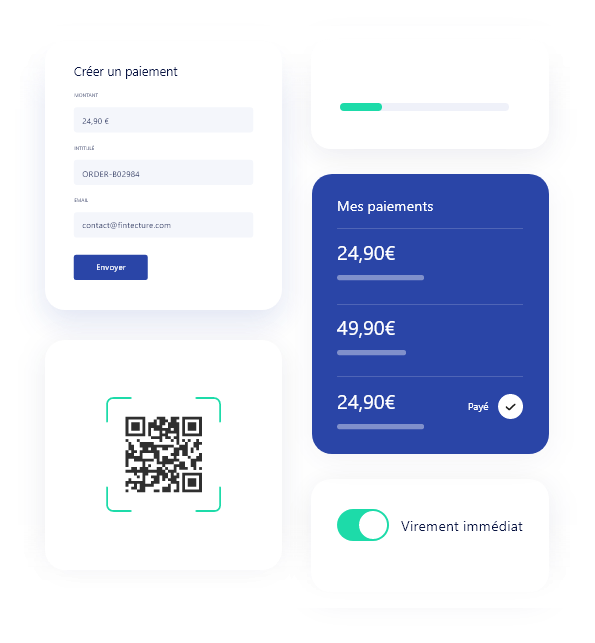

Fintecture, the bank transfer payment solution

DSO (Days Sales Outstanding) indicates the average time taken to pay customers. A high DSO lengthens the settlement time, impacting the company's cash flow.

Find out how Fintecture fights money transfer fraud. Risks, consequences and solutions to secure your transactions.

Find out how Fintecture's payment by transfer optimizes donation collection. Simplify the process, increase conversions.