Instant money transfer explained: Speed, rates and advantages

Discover instant money transfer in France: fast, secure payments. Complete guide to rates and compatible banks.

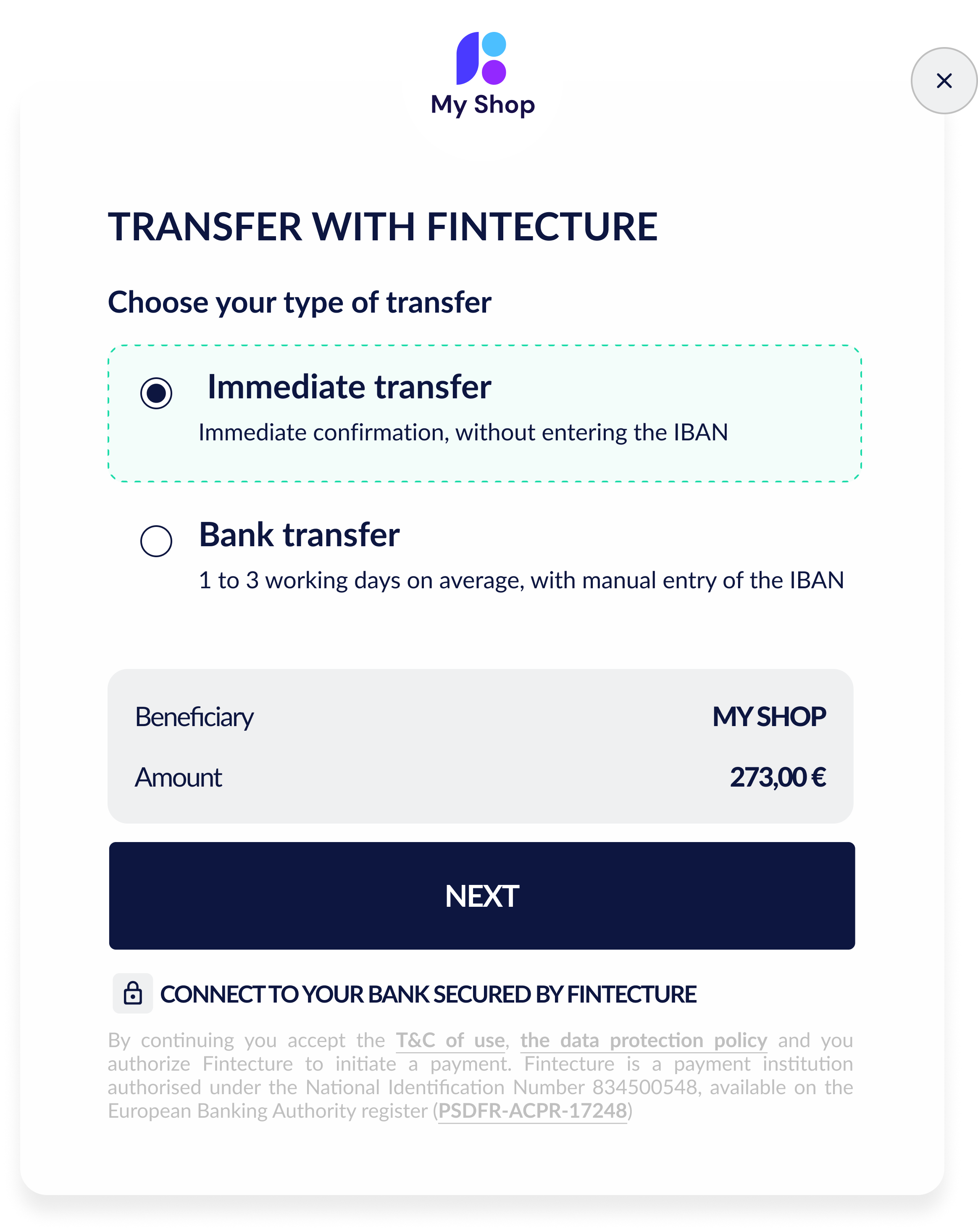

Fintecture, the bank transfer payment solution

Discover instant money transfer in France: fast, secure payments. Complete guide to rates and compatible banks.

One third of the companies that have been victims of fraud have suffered losses of more than 10,000 euros and 14% more than 100,000 euros. Fraud is thus a major issue for the financial stability of companies.

Explore the future of payments with Verifone and Fintecture. Innovative bank transfer solutions await you. #partnership